Quantifying Geopolitical Risk: The Impact of EU Anti-Dumping Measures

The European Union has confirmed the imposition of anti-dumping duties reaching up to 60.3% on specific imported goods. This dramatic tariff escalation necessitates an immediate reassessment of sourcing strategies for affected commodities.

These tariffs are designed to counter alleged unfair trade practices, but their immediate effect is profound trade contraction and export uncertainty. Analysis of historical trade data indicates that such high duties lead to significant reductions in export volume, compelling businesses to:

- Diversify Manufacturing Bases: Companies heavily reliant on the affected trade lanes must expedite plans to shift production to non-EU tariff zones.

- Re-evaluate CIF Costs: The effective landed cost of goods subject to these duties renders previous procurement models non-viable, demanding rapid price adjustments or substitution strategies.

Carrier Cost Pressure: The Resurgence of US West Coast PSS

Effective late February, a major global carrier announced a standardized Peak Season Surcharge (PSS) of $1,000 per standard container equivalent (FEU) for all shipments routed to US West Coast and Canada West Coast ports.

While some previously announced PSS applications were temporarily suspended, the implementation of this new, uniform charge signals a market shift. Carriers are proactively managing capacity deployment and leveraging demand spikes related to pre-Lunar New Year rushes and anticipated early Q2 inventory replenishment.

The $1,000 PSS is defined as separate from base ocean freight and other standard surcharges (e.g., BAF/CAF). LMLC advises shippers to immediately adjust logistics budgets and negotiate long-term fixed rates where possible to mitigate unexpected quarter-to-quarter financial exposure.

Macroeconomic Headwinds: Strategic Implications of Slower Retail Growth

Forecasts for 2026 anticipate a general slowdown in retail growth across major European and US markets. Key projected growth rates are notably lower than in previous periods:

- United States: 2.6% - 3.0%

- United Kingdom: 2.0%

- France: 1.5%

- Germany: 2.5%

This slowdown is attributed to persistent geopolitical instability, a cooling labor market, and increased consumer pressure from high costs of living. Consumers are increasingly prioritizing value, leading to a surge in demand for lower-priced goods and private-label brands.

For logistics providers and shippers, this trend reinforces the mandate for operational efficiency. The strategic optimization observed at major e-commerce platforms—such as large-scale corporate workforce reductions aimed at streamlining management and increasing execution efficiency—reflects the industry-wide focus on maximizing productivity per employee and reducing structural complexity ahead of tighter retail margins.

LMLC maintains that agility in adapting inventory levels to localized consumer behavior and strengthening digital system integration will be the primary determinants of competitive advantage in this tightening economic landscape.

-

Mitigating 3PL Billing Opacity: A Strategic Framework for Cost Control

The pervasive complexity of Third-Party Logistics (3PL) invoices leads to significant cost creep and threatens profit margins for growing businesses. Lack of standardization and detailed itemization often results in clients paying for unverified or unused services. LMLC recommends implementing automated invoice auditing protocols and mandating transparent cost-code mapping during contract negotiation to restore financial clarity.

2026-02-09

-

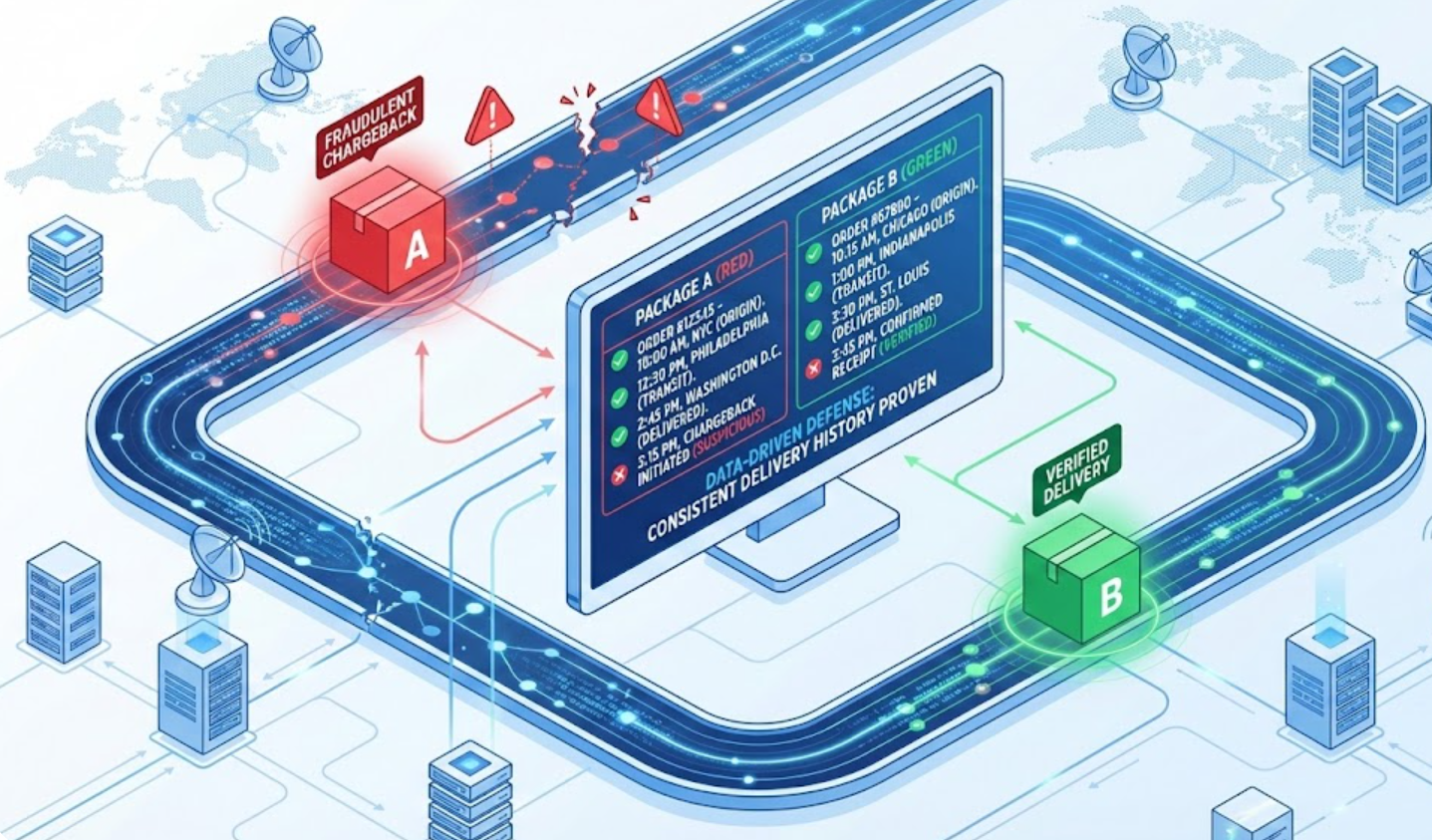

Mitigating Second-Order Chargeback Fraud: Logistics Data as the Ultimate E-commerce Defense

The rise of sophisticated e-commerce chargeback fraud, specifically schemes involving immediate follow-up orders, poses a significant threat to Shopify sellers. This fraud pattern is designed to exploit seller trust while attempting to defraud the initial transaction. Leveraging granular, immutable logistics tracking data is critical for validating delivery claims and successfully contesting fraudulent disputes.

2026-02-06